Owning your own business can be a dream come true for many, and not without reason. Perhaps you are finally bringing an idea you have had for years to life, or are simply seeking more flexibility and a change from the standard daily routine.

While it is often rewarding, it is not without risks, especially in the current economic climate. Many small businesses are only just starting to get back on their feet after the worst double-dip recession in 50 years.

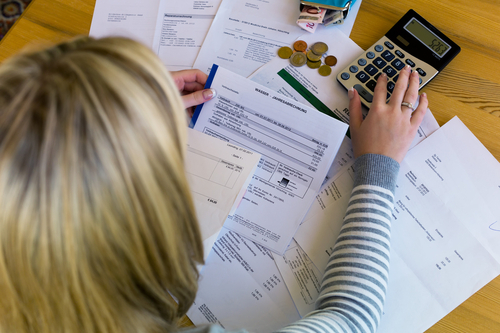

Managing cash flow is one of the main challenges faced by any small businesses today. In an ideal world, the money you receive for supplying goods and services is used to pay creditors as soon as possible. However, it is not always that straightforward.

Insolvency occurs when a company’s liabilities exceed its assets, when the debtor is unable to pay its creditors. In a small business, insolvency can be as a result of something simple. Perhaps your main supplier ceased trading? Your biggest client goes into liquidation? Raw materials become too expensive due to inflation? Changes in regulation threaten the whole operation of your business? The list is endless.

If you are struggling to meet the repeated demands of your creditors, and the resources aren’t available to improve the situation, business insolvency could present a real threat. Arming yourself with the right knowledge of the risks small businesses face is the best way to prepare for any challenges in the future.

As the director of a limited liability company you have limited liability, and so personal assets will not be at risk when your business is struggling to pay off its debts. However, if you turn a blind eye to the situation and continue to trade, you may be personally liable for a portion of the money owed and deemed unsuitable to act as company director for up to 15 years.

There are a number of solutions available to directors facing insolvency:

Company Voluntary Arrangement (CVA) – Where a repayment plan is agreed by your creditors and portion of your debt is written off, allowing you to continue trading.

Liquidation – Where a company ceases trading, all assets are sold in order to pay creditors/liquidation fees and expenses. Any remaining assets are divided between shareholders.

Informal Arrangement – This is where a company agrees to a repayment plan with the creditors, absent of any third party involvement.

Administration Order – This is an insolvency procedure which protects a company from its creditors, enabling it to continue trading.

See also: How to wind up a small business – a step-by-step guide

If you are able to spot the signs of financial pressures in the company early on, the sooner you can implement the correct adjustments and measures to ensure successful and continued trading.