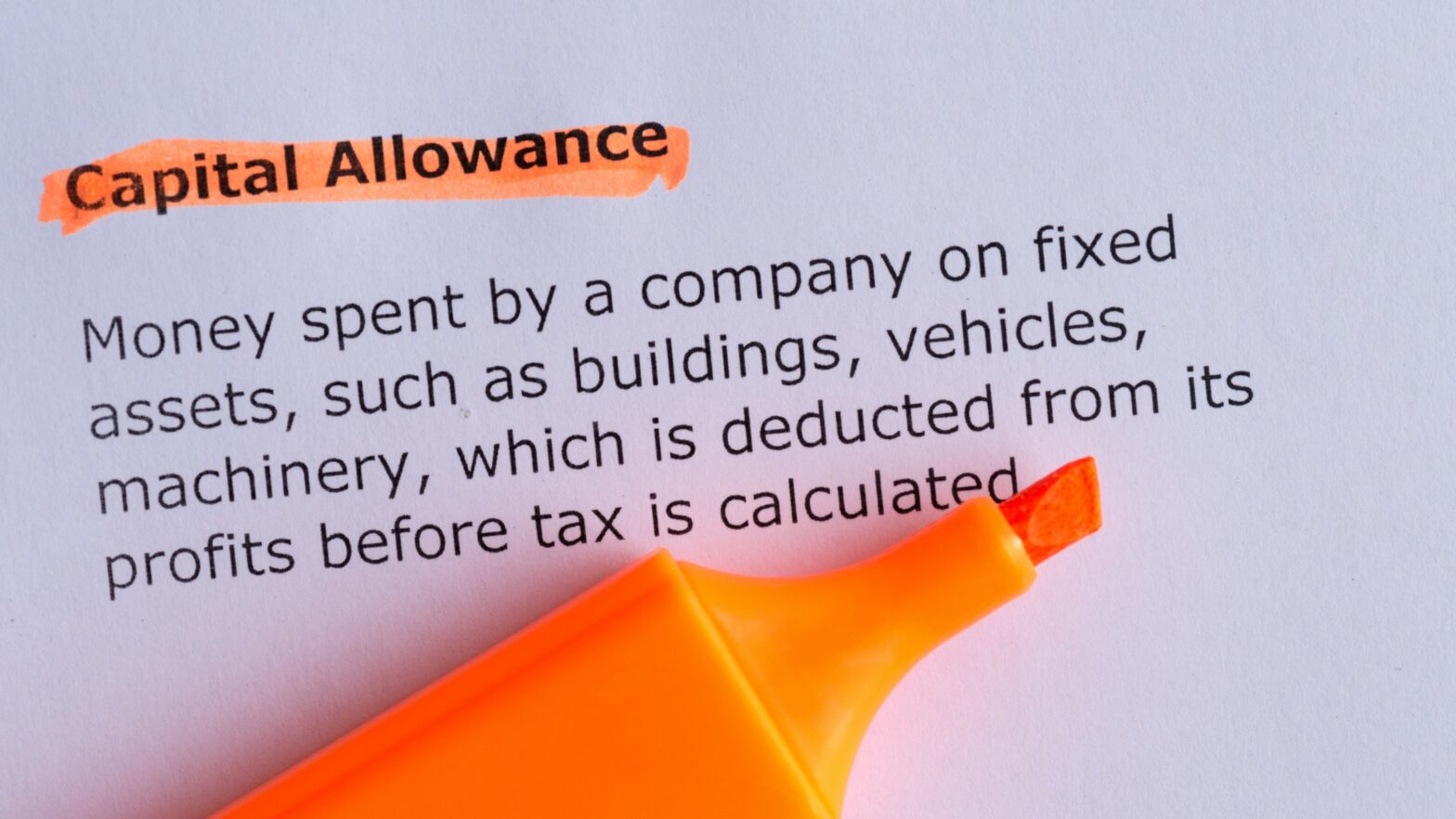

Capital allowances are available on qualifying capital expenditure incurred on the provision of certain assets used in a company or individual’s trade. Not all assets qualify for a capital allowance and the rate of relief will vary. The allowances are deducted from trading profits effectively reducing the tax payable. This would be the income tax for a sole trader or partnership and corporation tax for a company.

In most cases, items purchased which are allocated as “plant and machinery” would achieve 100 per cent relief via the Annual Investment Allowance (AIA). The current AIA limit is £1,000,000.

HMRC is generous in what it considers qualifying expenditure and includes:

- Computer equipment and servers

- Tractors, lorries, vans

- Ladders, drills, cranes

- Office chairs and desks

- Electric vehicle charge points

- Refrigeration units

- Compressors

However, certain items, such as cars, and items owned before you started a business and items given to you or your business are ineligible for this AIA claim. You would only be able to claim writing down allowances via the main pool and special rate pool with a lower percentage claimed. The main pool is where the majority of your “plant and machinery” assets will go to once AIA has been utilised first. The special rate pool will include your integral features, items with long life, thermal insulation and certain cars with CO2 emissions over a certain threshold.

Ineligible for capital allowance

There are other items which are ineligible for capital allowances entirely but one of the most complex areas relates to buildings and development expenditure. Here, capital allowances claims are often understated, meaning companies are missing out on significant savings due to missing qualifying expenditure that is eligible for a claim.

Certain expenditure on a building can be classified as plant and machinery under “integral features” which attracts a higher rate of capital allowance than a building. This includes items such as lifts, water heating systems, air conditioning and lighting systems.

Then there are items that are ineligible for capital allowances which includes things you lease on finance, and parts of buildings including doors, gates, mains water and gas systems, and land and structures. The rules regarding what expenditure qualifies as plant and machinery are very complex and are derived largely from case law.

It is not uncommon for businesses to think some items would be ineligible only to find they are eligible under the structures and building allowance, which includes claims on the construction costs such as design fees, renovation, repair, conversion and fitting out works.

Also, it is not uncommon for the costs of a building attributable to the items allowable as plant and machinery to be lost in the overall cost of the building making it very difficult to separate these assets out. Businesses are advised to use a chartered surveyor and/or accountant who is familiar with the qualifying expenditure rules to assist in identifying the costs eligible, checking that the building qualifies, and no previous claims have already been made on the expenditure. They can also make a claim on behalf of you.

Super-deduction

The UK government in its March 2021 Budget introduced a temporary super-deduction capital allowance for companies whereby they can claim 130 per cent on qualifying new capital assets between the period of the 1 April 2021 and 31 March 2023. This is to help encourage companies to invest in their productivity and competitiveness. So if you are company debating on whether to buy that new piece of machinery or update your computer equipment then it may be a good time to do this. Again, please do speak to an accountant to make sure the assets you are thinking of buying are eligible for the super-deduction claim.

Toby Cotton is a manager in the business services team at accountants, business and financial advisers Kreston Reeves

Further reading

Super-deduction tax break – what is it and how does it work?